For Week Ending October 7, 2017

Many potential buyers are simply not on the market during this time of year, as school-aged children settle into routines and the gainfully employed focus more on end-of-year goals and holiday planning over taking on a big move. But not all buyers are equal. Consider instead the first-time buyers with no children, relocated employees, investment buyers, bargain hunters and those with generally fewer ties to established routines.

In the Twin Cities region, for the week ending October 7:

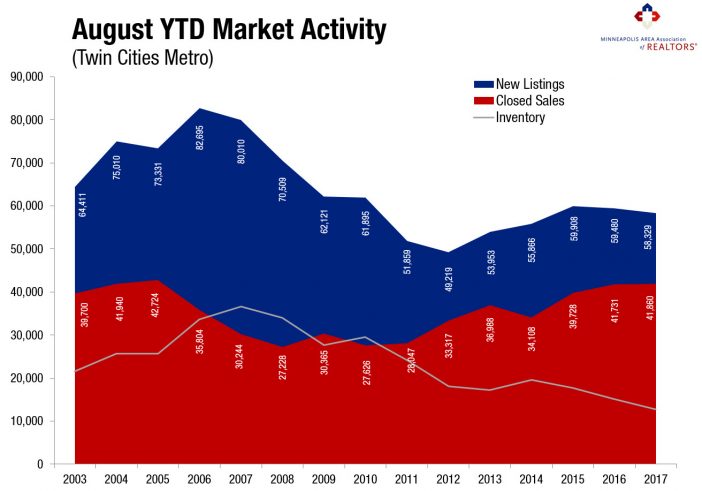

- New Listings decreased 1.3% to 1,395

- Pending Sales increased 4.1% to 1,103

- Inventory decreased 16.6% to 12,378

For the month of September:

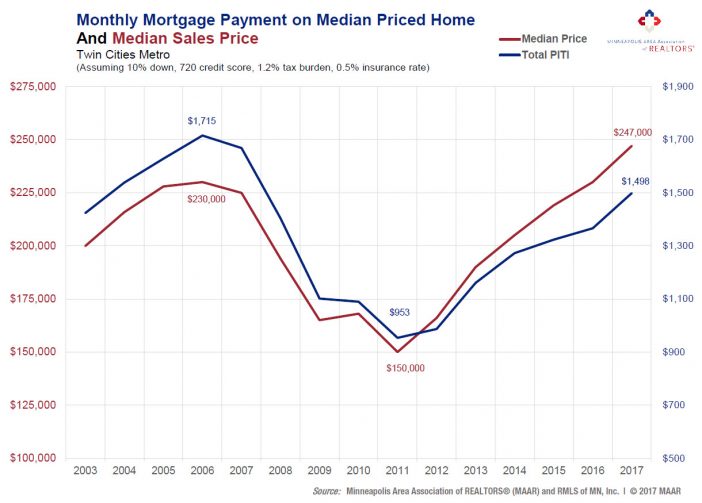

- Median Sales Price increased 7.3% to $246,800

- Days on Market decreased 12.3% to 50

- Percent of Original List Price Received increased 0.6% to 98.1%

- Months Supply of Inventory decreased 16.7% to 2.5

All comparisons are to 2016

Click here for the full Weekly Market Activity Report. From The Skinny Blog.